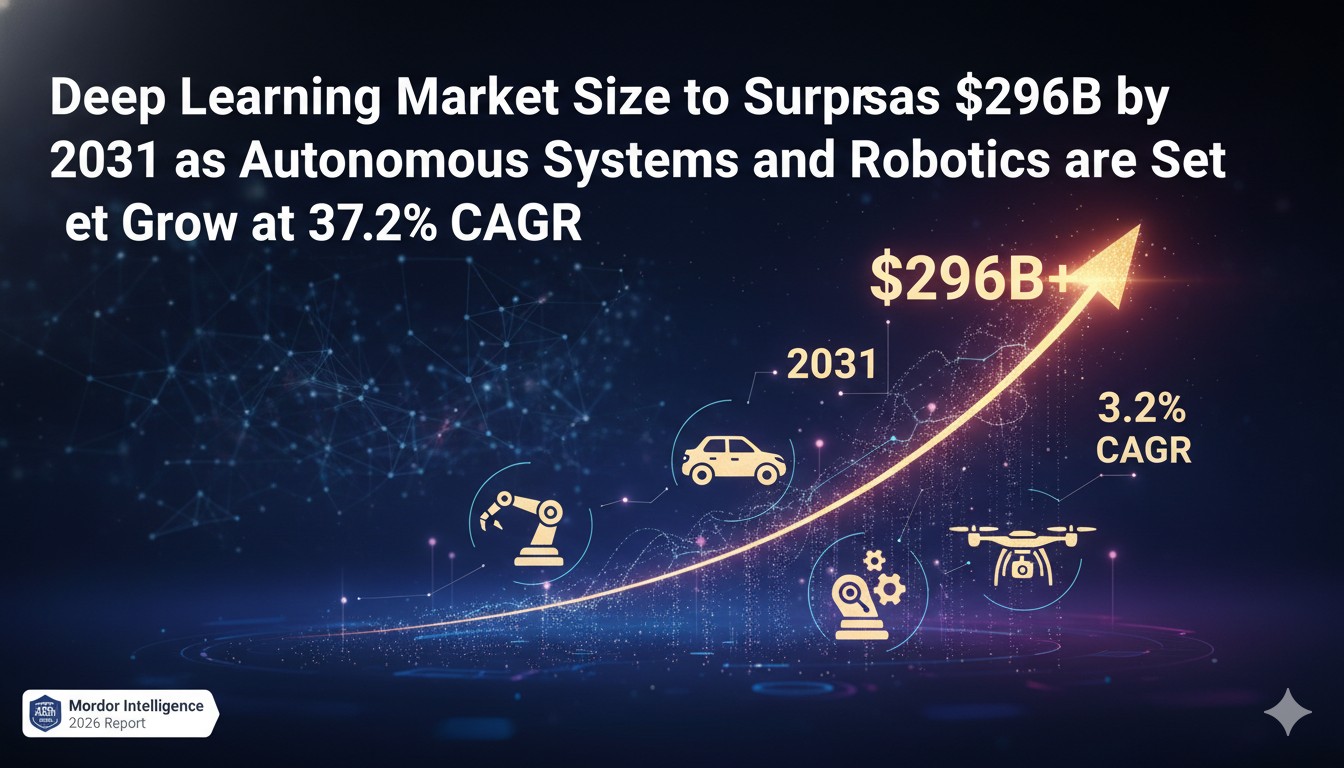

The global deep learning market, valued at approximately $64.92 billion in 2026, is on track to surpass $296 billion by 2031, expanding at a robust compound annual growth rate (CAGR) of 35.48%. This surge is fueled by widespread enterprise adoption of AI technologies, breakthroughs in generative AI, and surging demand for automation in computer vision, natural language processing, and especially autonomous systems and robotics, which are advancing at an even faster 37.2% CAGR. Hardware advancements, cloud integration, and cross-industry applications are accelerating deployment, though challenges like energy consumption and talent gaps persist.

Deep Learning’s Meteoric Rise Amid AI Transformation

The deep learning sector stands at the forefront of the broader artificial intelligence revolution, powering everything from image recognition to complex decision-making in real-world environments. As enterprises shift from experimental pilots to production-scale implementations, the technology has moved beyond research labs into core business operations. Financial services use it for fraud detection and algorithmic trading, healthcare leverages convolutional neural networks for diagnostic imaging, and manufacturing applies it to predictive maintenance and quality control.

A key highlight is the outsized role of autonomous systems and robotics. This application segment is projected to grow at a 37.2% CAGR through 2031, outpacing the overall market. Advancements in foundation models enable humanoid robots to handle context-aware tasks in warehouses, elder care, and logistics. Delivery bots now navigate dense urban environments with minimal human oversight, while collaborative robots—or cobots—learn new assembly sequences from limited demonstrations, addressing persistent labor shortages in factories.

Hardware accelerators, including specialized GPUs and TPUs, have dramatically reduced inference latencies for massive models. Transformer architectures, originally developed for language tasks, now underpin multimodal systems that process video, audio, and sensor data simultaneously. These innovations lower barriers for mid-sized companies, allowing faster integration without massive upfront infrastructure investments.

Cloud providers and specialized AI platforms have formed ecosystems that streamline deployment. Enterprises benefit from pre-trained models, automated scaling, and managed services that cut development cycles from months to weeks. Generative AI investments further amplify momentum, as organizations experiment with synthetic data generation to train robust models where real-world labeled data is scarce or expensive.

Despite the optimistic trajectory, several headwinds remain. Energy demands of training large-scale models strain power grids and raise sustainability concerns, prompting a push toward efficient architectures and green data centers. Regulatory frameworks around data privacy, bias mitigation, and AI safety are evolving rapidly, requiring compliance investments. A persistent shortage of skilled practitioners in model tuning, deployment, and ethical oversight also constrains scaling in some regions.

Market Segmentation and Regional Insights

By component, software tools and frameworks continue to dominate due to their flexibility and rapid iteration capabilities. Hardware, however, grows quickly as custom silicon optimizes for specific workloads like edge inference in robotics.

Deployment modes show a hybrid pattern: public cloud leads for scalability and access to vast compute resources, while on-premise and hybrid setups gain traction among organizations prioritizing data sovereignty and latency-sensitive applications.

Regionally, North America maintains leadership thanks to concentrated tech giants, venture funding, and early enterprise adoption. Asia-Pacific emerges as the fastest-growing area, driven by national AI strategies in China, Japan, South Korea, and India. These countries invest heavily in localized models, industrial automation, and robotics to boost manufacturing competitiveness.

Europe focuses on regulated sectors like automotive and healthcare, where explainable AI and compliance drive demand for trustworthy deep learning solutions.

Key Applications Driving Momentum

Image and Video Recognition — Remains the largest segment, powering surveillance, retail analytics, and medical diagnostics with high accuracy.

Natural Language Processing and Text Analytics — Fuels chatbots, sentiment analysis, and content generation tools amid the generative AI boom.

Autonomous Systems and Robotics — The standout performer at 37.2% CAGR, enabling perception, path planning, and manipulation in self-driving vehicles, drones, and industrial arms.

Other Areas — Including signal processing, recommendation engines, and anomaly detection across finance and cybersecurity.

Challenges and Future Outlook

While growth appears unstoppable, balancing performance with efficiency will define the next phase. Edge computing addresses latency and privacy by running models closer to data sources, particularly valuable in robotics and IoT. Federated learning techniques allow collaborative training without centralizing sensitive data.

As models grow larger, techniques like quantization, pruning, and knowledge distillation become essential to maintain speed and reduce costs. The industry also sees increasing emphasis on multimodal integration, where deep learning combines vision, language, and action for more capable autonomous agents.

The deep learning market’s trajectory underscores a broader shift toward intelligent, adaptive systems that enhance productivity and innovation across the economy. With autonomous robotics leading the charge, the technology promises to reshape industries in profound ways over the coming years.

Disclaimer: This is a news and analysis report based on industry trends and market projections. It is for informational purposes only and does not constitute financial, investment, or professional advice.